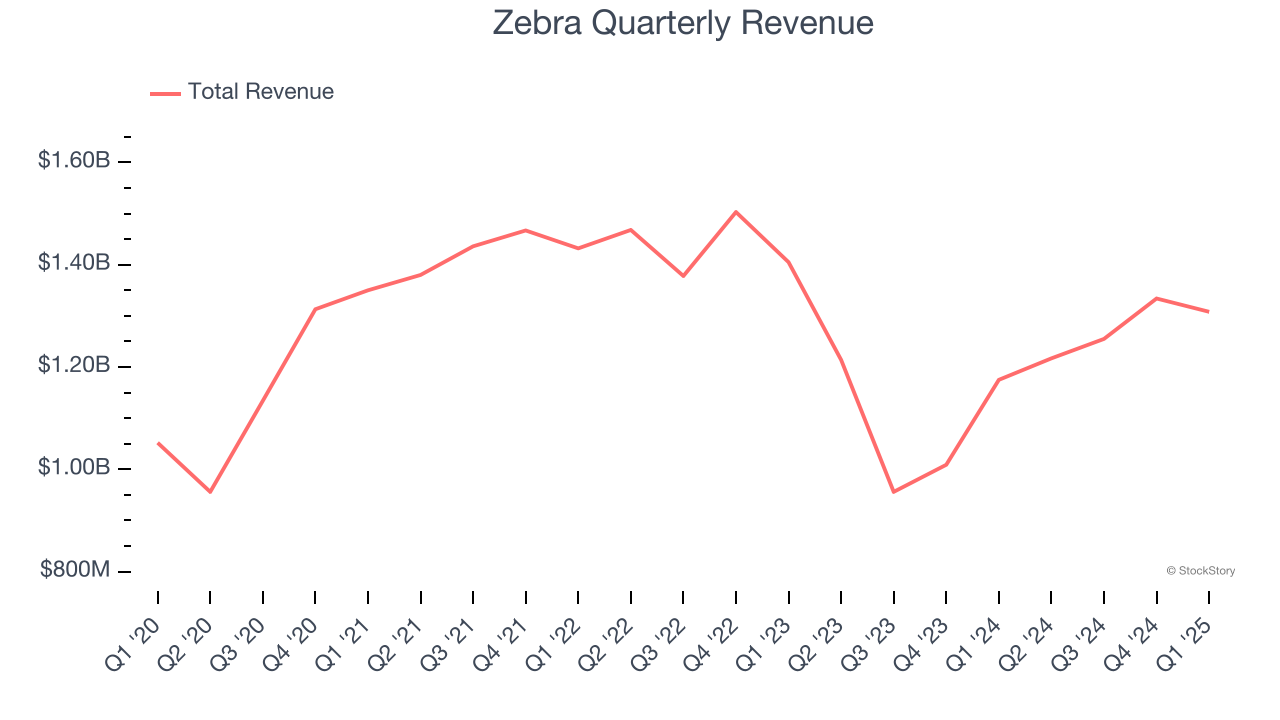

Enterprise data capture company Zebra Technologies (NASDAQ:ZBRA) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 11.3% year on year to $1.31 billion. The company expects next quarter’s revenue to be around $1.28 billion, close to analysts’ estimates. Its non-GAAP profit of $4.02 per share was 11.1% above analysts’ consensus estimates.

Is now the time to buy Zebra? Find out by accessing our full research report, it’s free.

Zebra (ZBRA) Q1 CY2025 Highlights:

- Revenue: $1.31 billion vs analyst estimates of $1.29 billion (11.3% year-on-year growth, 1.4% beat)

- Adjusted EPS: $4.02 vs analyst estimates of $3.62 (11.1% beat)

- Adjusted EBITDA: $292 million vs analyst estimates of $270.6 million (22.3% margin, 7.9% beat)

- Revenue Guidance for Q2 CY2025 is $1.28 billion at the midpoint, roughly in line with what analysts were expecting

- Management lowered its full-year Adjusted EPS guidance to $14.25 at the midpoint, a 5% decrease

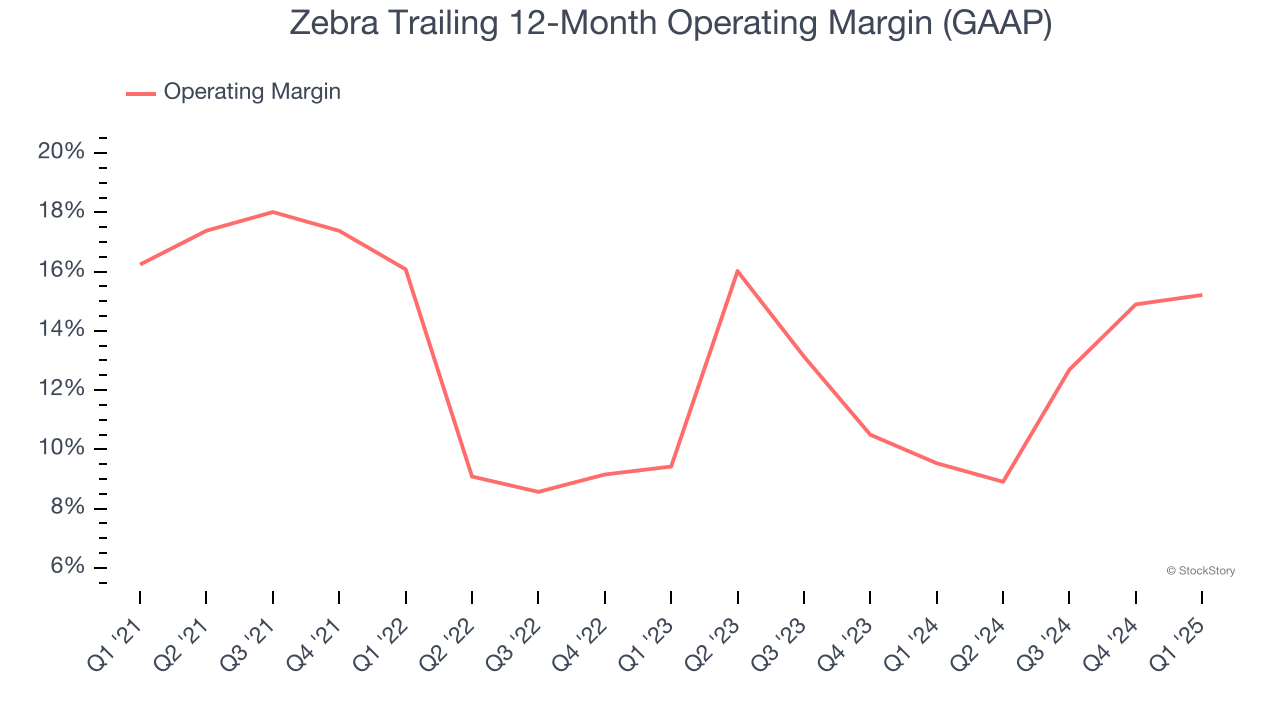

- Operating Margin: 14.9%, up from 13.5% in the same quarter last year

- Free Cash Flow Margin: 12.1%, up from 9.4% in the same quarter last year

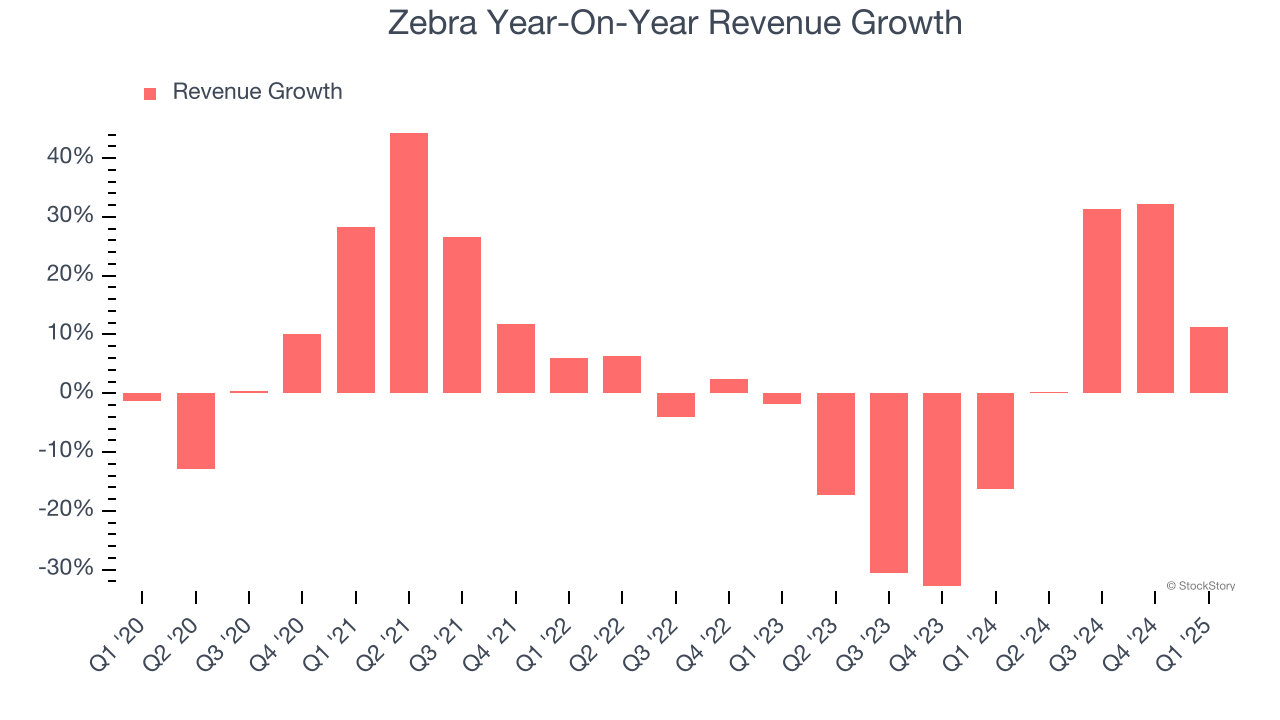

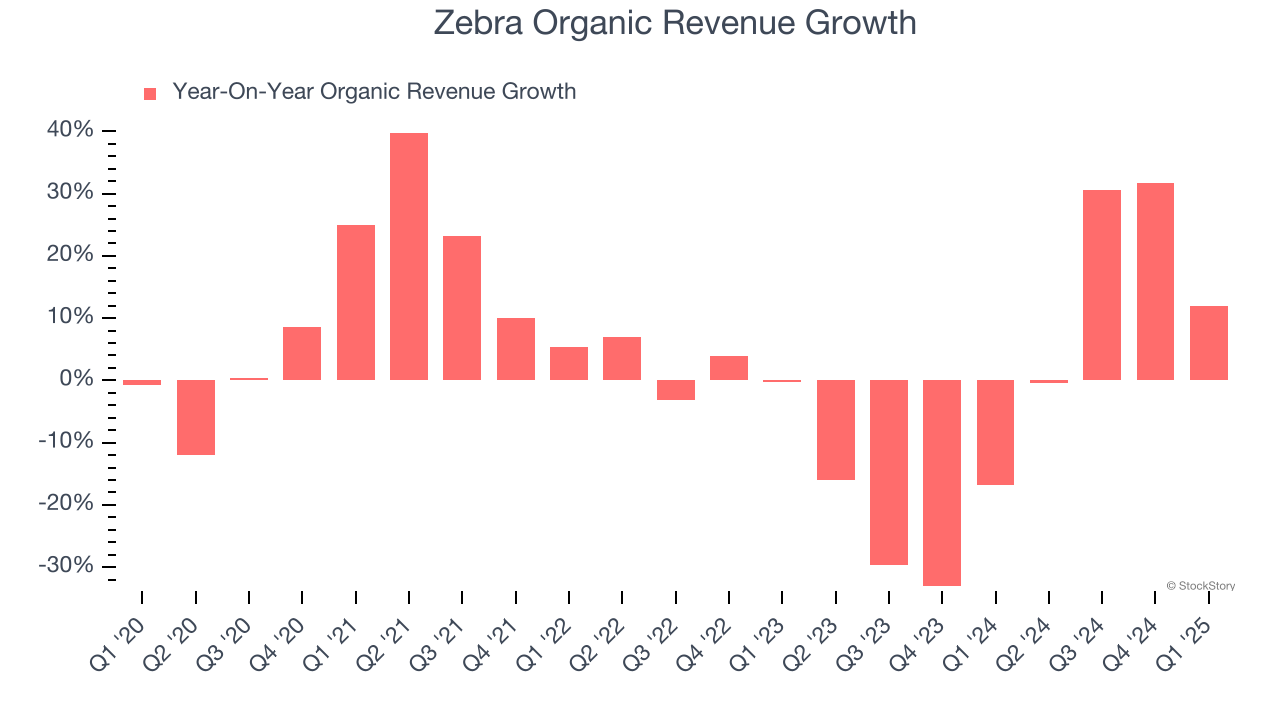

- Organic Revenue rose 11.9% year on year (-16.8% in the same quarter last year)

- Market Capitalization: $12.45 billion

“We delivered first quarter sales and earnings results above the high end of our outlook, reflecting strong demand, supported by our team's excellent execution," said Bill Burns, Chief Executive Officer of Zebra Technologies.

Company Overview

Taking its name from the black and white stripes of barcodes, Zebra Technologies (NASDAQ:ZBRA) provides barcode scanners, mobile computers, RFID systems, and other data capture technologies that help businesses track assets and optimize operations.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $5.11 billion in revenue over the past 12 months, Zebra is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, Zebra likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, Zebra’s 2.7% annualized revenue growth over the last five years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Zebra’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.7% annually.

Zebra also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Zebra’s organic revenue averaged 2.7% year-on-year declines. Because this number is better than its normal revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Zebra reported year-on-year revenue growth of 11.3%, and its $1.31 billion of revenue exceeded Wall Street’s estimates by 1.4%. Company management is currently guiding for a 5.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Zebra has managed its cost base well over the last five years. It demonstrated solid profitability for a business services business, producing an average operating margin of 13.3%.

Analyzing the trend in its profitability, Zebra’s operating margin decreased by 1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Zebra generated an operating profit margin of 14.9%, up 1.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

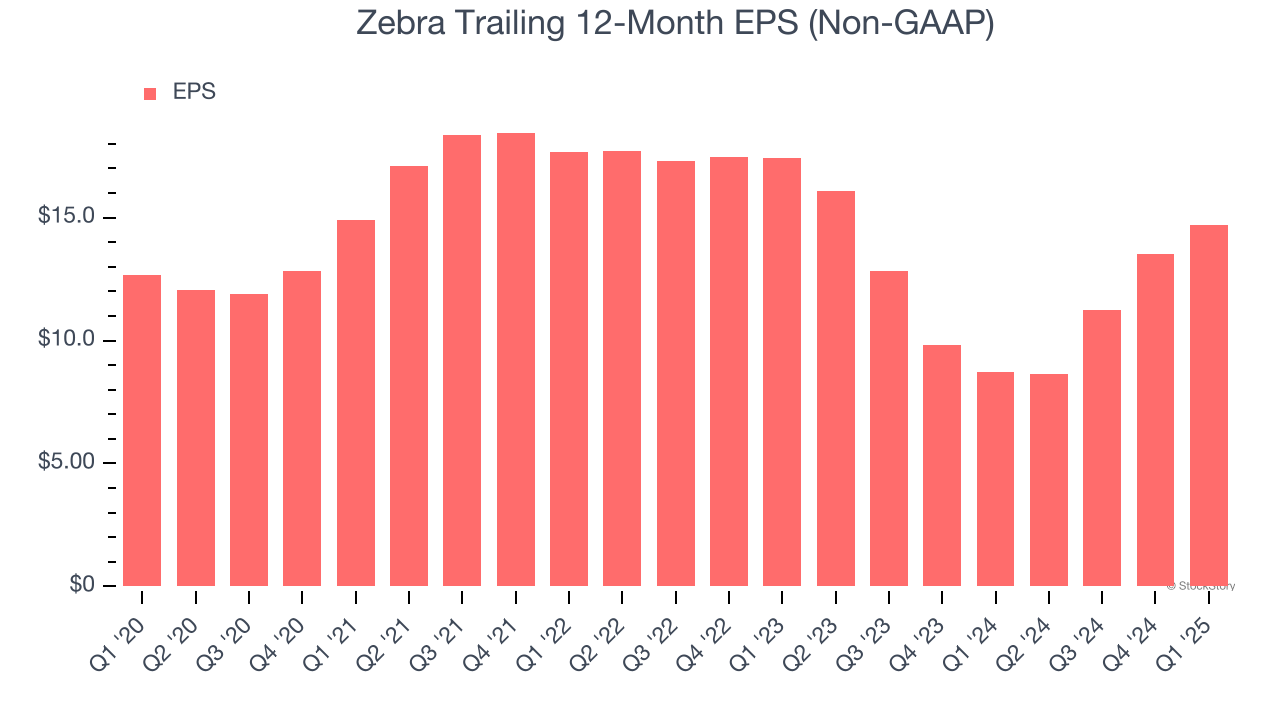

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Zebra’s weak 3% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Zebra reported EPS at $4.02, up from $2.84 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Zebra’s full-year EPS of $14.69 to grow 5.1%.

Key Takeaways from Zebra’s Q1 Results

We enjoyed seeing Zebra beat analysts’ organic revenue and EPS expectations this quarter. On the other hand, its EPS guidance for next quarter and the full year fell short of Wall Street’s estimates. Overall, this was a mixed quarter, but the market seems to be rewarding the strong quarter and overlooking the tepid guidance. The stock traded up 5.9% to $258.02 immediately after reporting.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.