West Pharmaceutical Services has gotten torched over the last six months - since October 2024, its stock price has dropped 29.3% to $202.47 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy West Pharmaceutical Services, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we don't have much confidence in West Pharmaceutical Services. Here are three reasons why there are better opportunities than WST and a stock we'd rather own.

Why Is West Pharmaceutical Services Not Exciting?

Founded in 1923 and serving as a critical link in the pharmaceutical supply chain, West Pharmaceutical Services (NYSE:WST) manufactures specialized packaging, containment systems, and delivery devices for injectable drugs and healthcare products.

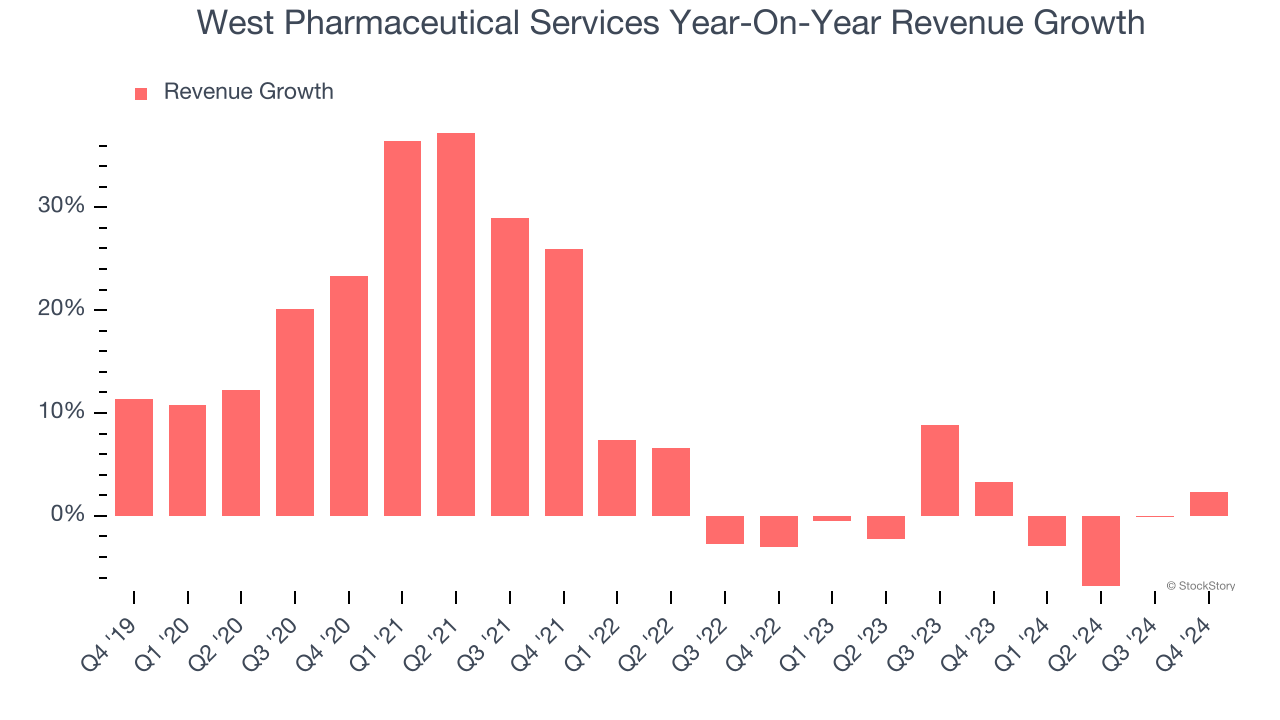

1. Revenue Growth Flatlining

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. West Pharmaceutical Services’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

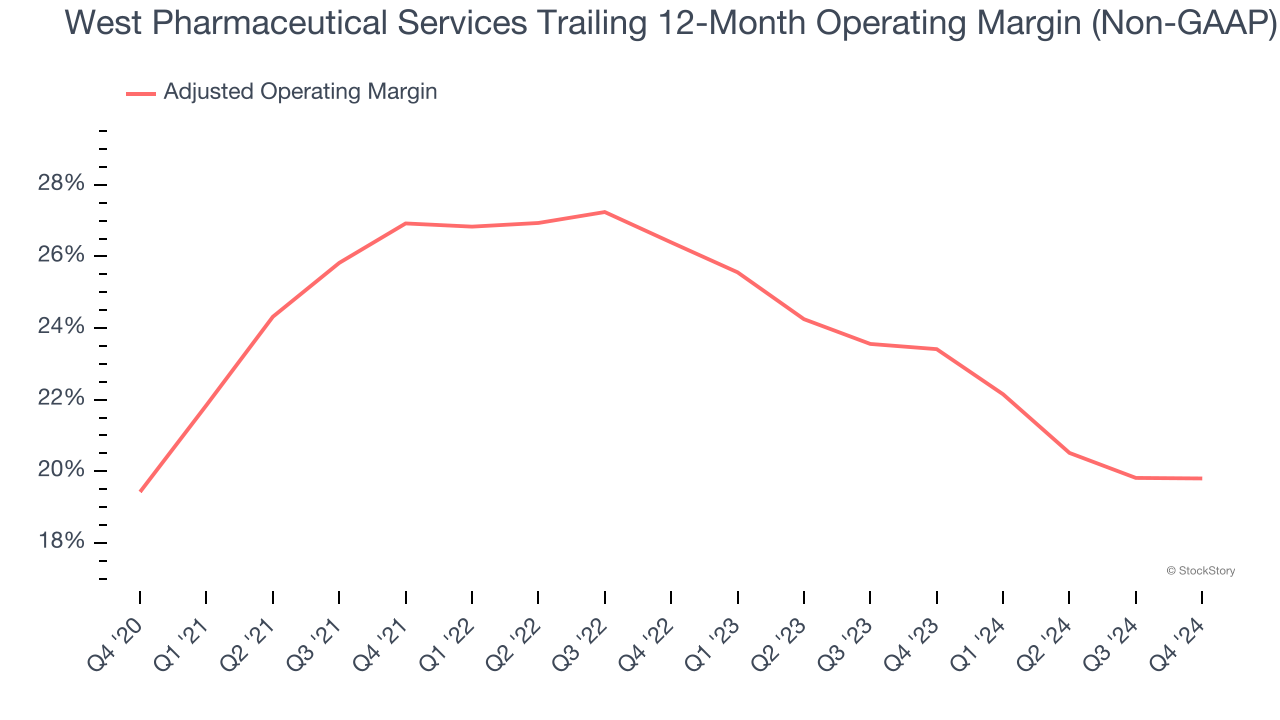

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Looking at the trend in its profitability, West Pharmaceutical Services’s adjusted operating margin decreased by 6.6 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 19.8%.

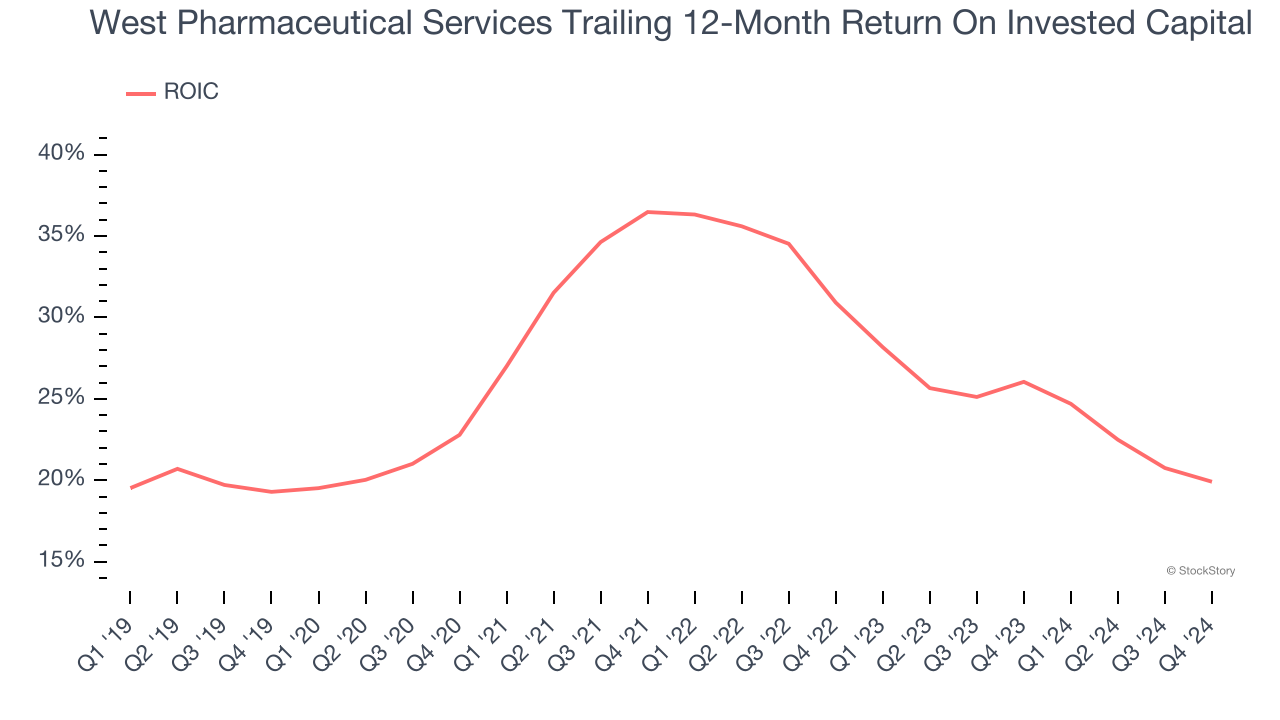

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, West Pharmaceutical Services’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

West Pharmaceutical Services isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 27.3× forward price-to-earnings (or $202.47 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of West Pharmaceutical Services

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.